- Home »

- Inform »

- Markets »

- Market outlook »

- Market outlook - November 2024

to read

US election likely to lead to a change of favourites in equities

#1 Market & Macro

- October proved to be a poor month for investors, on stock and bond markets alike. The S&P 500, usually breaking record after record, experienced the first negative month in six months, and 10-year US Treasuries lost four percent on the bond market.

- “Public debt has obviously made inroads in the minds of investors”, Björn Jesch, global DWS Chief Investment Officer, states. This has become obvious in both, the United States, where concerns of ever increasing public debt have markedly pushed up rates for long maturities, and in the United Kingdom.

- In face of an expected rate-cutting cycle by central banks, Jesch remains strategically constructive on corporate bonds. “However, we have downgraded our long-term favorites – investment-grade European corporate bonds – tactically, i.e. short-term, to ‘neutral’ since there is hardly any scope for a tightening of spreads to sovereign bonds.”

-

With a view to stocks, Jesch expects changes after Donald Trump winning the US presidential election to be of minor importance for the overall market than for individual sectors. “However, if 10-year Treasury yields start moving towards five percent, this could create strong headwinds for stocks,” Jesch adds.

-

Investors now must decide whether they prioritize the fear of higher inflation and thus fewer interest rate cuts by the Fed or the expected more business-friendly policies of Donald Trump.

A further reduction of corporate taxes could boost S&P500 profits by 3 to 4 percent, however not before 2026, Jesch cautions. Corporations with a high share of domestic, i.e. US profits, would benefit most. These are mainly in the financial sector or in the market segment of small- to mid-caps. - Markets outside the United States are, however, at least for the time being, facing rough times due to the unpredictability of the incoming President, the DWS chief investment officer expects.

Topics driving capital markets

Economy: decent growth in the United States, Spain particularly strong in the Eurozone

- Consumption continues to drive the US economy. The annualized growth rate for the third quarter is 2.8 percent after 3.0 percent in the second quarter.

- Growth rates from the Eurozone surprised slightly on the upside: the third quarter registered a plus of 0.4 percent (Q2: 0.2 percent). With a growth of 0.8 percent, the Spanish economy proved to be particularly strong, boosted by continuing tailwinds from tourism.

Inflation: prices have slightly risen again

—Eurozone inflation has risen to 2.0 percent in October (September: 1.7 percent). Core inflation – excluding food and energy – stayed at 2.7 percent.

—In Germany, the inflation rate rose to 2.0 percent in October (after 1.6 percent in September), driven by higher food and energy prices.

Central banks: further rate cuts expected

- In mid-October, the European Central Bank cut its key rates by 0.25 percent to 3.25 percent. We expect another rate cut in December.

- The Federal Reserve should continue to closely watch inflation. Its further rate path will depend on incoming data.

Risks: high stock-market valuations and geopolitical crises

- High valuations on stock markets might prove a factor substantially limiting further price potential – particularly since growth of corporate profits is slowing down towards historic averages.

- Apart from Russia’s war of aggression against Ukraine, the unstable situation in the Middle East is another spot of geopolitical concern, particularly the further escalating conflict between Iran and Israel.

Dividends could regain more importance for stock performance

#2 Equites

- Growth or value stocks – the question of favorites seems to be a rather rhetorical question. The past ten years have only recorded two years – 2016 and 2022 –, in which value stocks have taken the lead,” Thomas Schüßler, Co-Head Global Equities, states.

- The currently very high valuations, particularly of tech stocks, are far from being a reason of blocking a further upward path of these papers. Following the trend is the order of the day. This does, however, not mean that there are no good reasons for investing in value stocks, for example via a dividend strategy. Investors also appreciate good risk management since there will always be setbacks. Not every investor strives for maximum returns at maximum risk,” Schüßler argues.

- Particularly promising are dividend papers from the financial sector, utilities or oil corporations, which tend to have very high dividend ratios. Picking interesting dividend stocks on the US market is currently difficult. S&P 500 dividend returns of 1.2 percent are substantially underperforming the average of the past twenty years of 2.0 percent. Even if high valuations are not regarded as an indicator of an imminent slump, it can be assumed that shareholder returns of the next few years might fall short of their long-term average.

- “Looking through the windscreen, I rather see returns of five percent and not the eight or ten percent achieved in the past,” Schüßler comments. Current valuations could be seen as premature returns. They are far ahead of the current profits of corporations. This is another argument in favor of dividend stocks, the performance of which is based on both, dividends and price gains. With a view to the US market, the most important stock market of the world, Schüßler regards high public debt as a risk.

- Currently, public debt is still having a positive effect on the stock market. But high public debt in combination with a falling saving rate and rising debt of private households is a problematic constellation. “High private debt currently supports the stock market.

- People continue on their shopping sprees without forcing corporations to substantially increase wages,” Schüßler argues. But at some point, a threshold will be breached. This might result in rising bond yields, probably putting stock markets under pressure.

- Against the background of this rather risky situation on stock markets and the increased danger of setbacks, Schüßler is, apart from dividend stocks, also warming to gold and gold mining equities. “Diversification and capital protection are their major positive aspects,” Schüßler concludes.

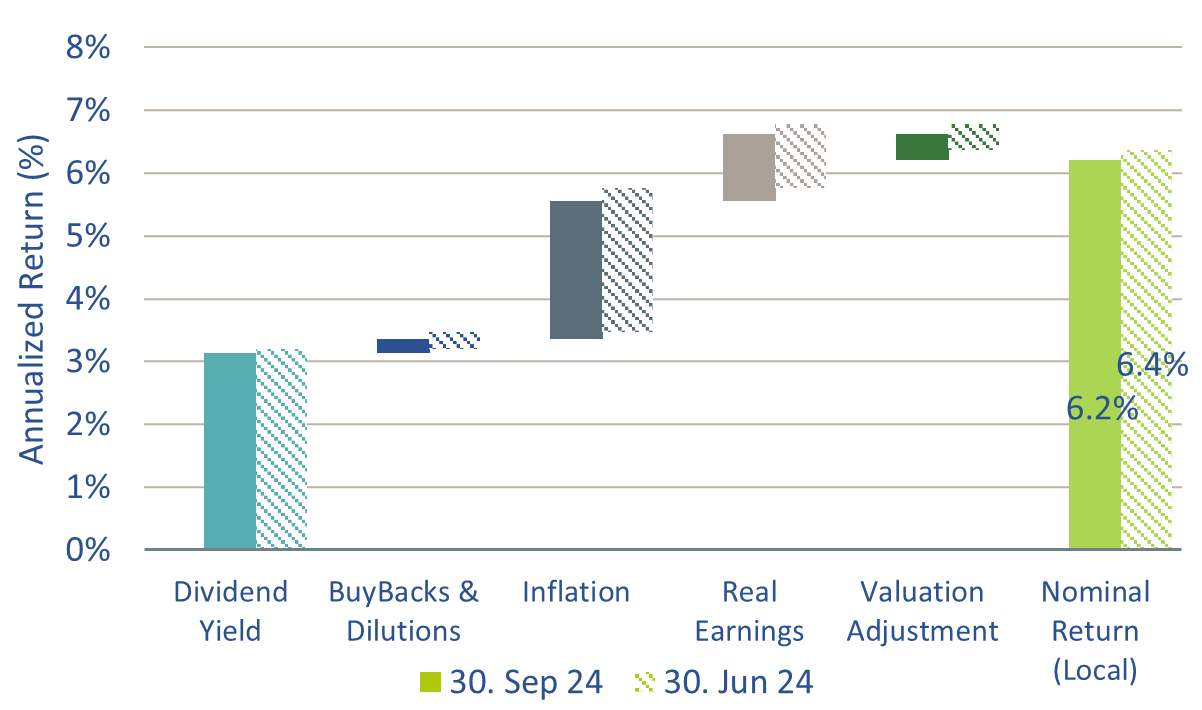

Dividend yields: an important part of total returns

Expected composition of stock returns

Source: DWS Investment GmbH, as of end of October 2024

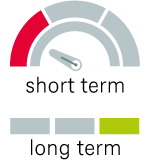

Equities USA

stronger focus on domestic corporations

|

|

Equities Germany

prices higher than warranted by fundamental data

|

|

|

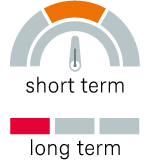

Equities Europe

implications of US election somewhat weaken the outlook

|

|

|

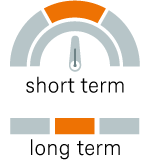

Equities Japan:

no turnaround of the Chinese stock market on the horizon yet

|

|

|

Short-term market setbacks offer opportunities in risky assets

#3 Fixed Income

- How will the numerous economic and geopolitical uncertainties impact the weighting of asset classes in a portfolio? “With a view to risk preferences, we remain neutrally positioned in our allocation portfolios, ”Henning Potstada, Global Head Multi-Asset, states.

- Potstada expects a further steepening of the yield curve so that the yield spread between long and short maturities will widen. “Moreover, in a market environment, in which growth concerns have replaced inflation concerns, duration should be able to contribute to portfolio stability,”

- Potstada explains. All in all, allocation portfolios will remain neutrally positioned with a view to fixed income although yield levels are all but unattractive compared with stocks. As to stocks, Potstada observes two opposing developments: “Our base scenario with rate cuts combined with the avoidance of a recession would warrant a positive assessment of stock markets.

-

But a further rally on stock markets could be contained by ambitious valuation levels – particularly in the United States – and a continuing weaker macroeconomic picture.” Generally, short-term market setbacks will offer entry points into high-risk assets.

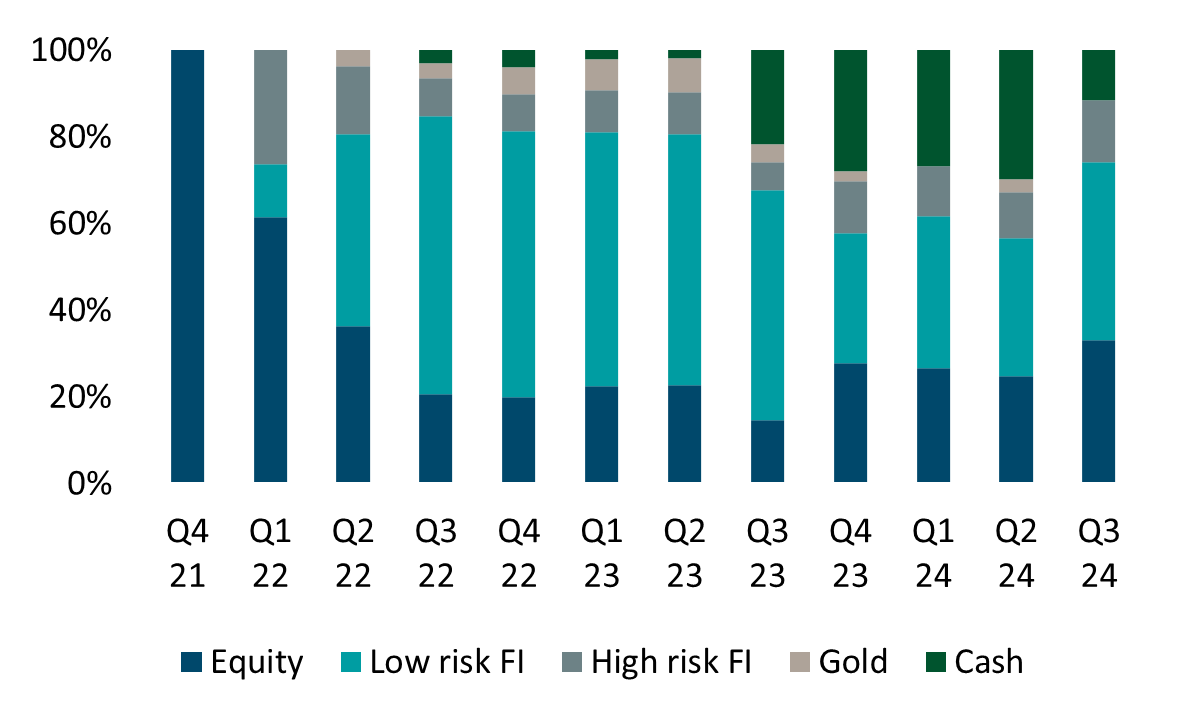

Bonds remain important yield earners

Sample allocation for a target return of four percent

Source: DWS Investment GmbH, as of end of September 2024

U.S. government bonds (10 years)

Yields set to rise again

|

|

|

German government bonds (10 years)

Yields should have peaked

|

|

Emerging market sovereign bonds

Tighter yield spreads – hardly attractive in the short run

|

|

Credit

Investment Grade

| |

|

High Yield

|

|

Euro/Dollar: Much uncertainty around the dollar, short-term rather somewhat stronger

#4 Currencies

|

|

|

Gold: handsome price gains in the year to-date – outlook should remain positive in the face of numerous uncertainties

#5 Alternative assets

|

|

LegendThe strategic view by September 2025 The indicators signal whether DWS expects the asset class in question to develop upwards, sideways or downwards. They indicate both the short-term and the long-term expected earnings potential for investors. Source: DWS Investment GmbH; CIO Office, as of 06 November 2024 DWS Market Outlook: The entire document can be found here. |

|

|

|

|

|

|

|